There are a lot of articles out there explaining various DeFi use-cases.

While I’ve found that a lot of these are quite interesting and will no doubt be very important, they are also quite nascent in terms of wider applicability to society at the moment. For example, most decentralized insurance protocols currently cover on-chain losses such as bridge hacks. Nexus Mutual plans to roll out additional decentralized coverages in the future such as earthquake insurance, but I consider these to still be a while away from gaining broader adoption.

The amount of funds within DeFi has grown to $55B, significantly higher than ~$700M in mid-2020. Despite a recent sell off, DeFi is here to stay and I expect more funds to enter the space in the not-too-distant future.

While all DeFi use cases are both interesting and relevant, below I’ll focus on some applications that I consider both personally of great interest, and also immediately beneficial to a wider audience.

This list is by no means exhaustive — please share any other applications you like in the comments!

1. Unlocking Liquidity Through Cryptocurrency Assets

The average American holds $185,000 in home equity, enabling them to use their real estate as collateral to access liquidity. There are other assets that can also be used as collateral such as vehicles, stock portfolios, and other comparable assets. The downside is that it is usually a time-consuming and legally complex process with limited transparency for the borrower.

In contrast, people globally can use their cryptocurrency assets as collateral to instantaneously take out loans from a global liquidity network. Various borrowing/lending protocols exist on each blockchain, with Aave being the largest on Ethereum and Venus Protocol being the largest on Binance Smart Chain. In the future, institutions will increasingly be able to do this for their investors as well, though this would not be decentralized.

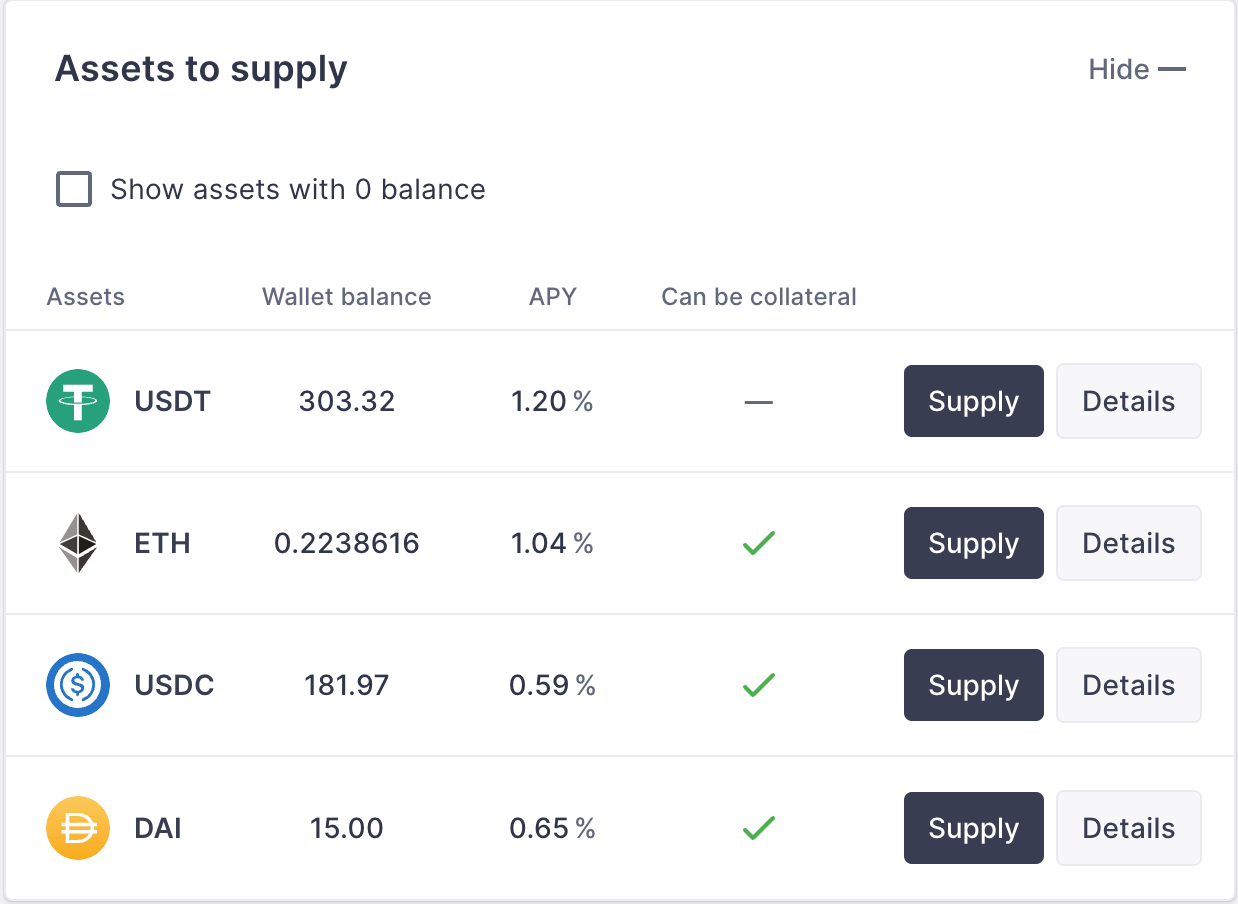

How does this work in practice? If I have $5,000 worth of Ether (or Bitcoin, BNB, etc) I could deposit these on a protocol such as Aave. It’s then locked up, and I’m paid an APY. Below, we can see I would be receive 1.20% for my USDT (better than any bank savings-account) and 1.04% on my Ethereum. These rates vary over time depending on liquidity, and by protocol used.

I could then borrow any asset of my choice, up to a certain ratio such as 80%. So I’m able to access liquidity while still benefitting to any upside potential of Ethereum.

The risk is the price of Ethereum falling below my collateral ratio. If I were to deposit $5,000 of Ethereum, and then borrow $3,000 of a stablecoin like USDC, my ratio would be 60% and the risk for me is that I get liquidated by Ethereum falling by 40% or greater.

For example, late-August 2022 saw prices of Bitcoin and Ethereum drop by ~6.8%, causing liquidations of over $300M.

2. Tokenization Of Assets

Tokenization is quite a broad field so I’ll only cover it at a high level. Tokenization refers to representing real-world assets on the blockchain.

A good example that I’ve already written about is in regards to tokenizing gold on the blockchain. There are significant issues with buying/selling physical gold, such as security, timeliness, intermediary costs, limited liquidity networks, and high minimum purchase amounts.

In contrast, it’s possible to issue the equivalent value online as gold-tokens which track the value of underlying gold that would be held by a regulated institution. In turn, anyone globally can instantaneously purchase any fraction of gold that they’d like ($2, or $2 million) with very low fees and underlying blockchain security.

This is comparable to USD-backed stablecoins which I’ll focus on next. These are simply tokenized USD’s which are held by regulated institutions for token holder redemption at any point.

While gold is fairly liquid, USD’s are extremely liquid, there are also many illiquid assets that could benefit from tokenization. In fact, Boston Consulting Group (BCG) estimates that the tokenization of illiquid assets will reach $16T by 2030.

Unlocking liquidity in illiquid assets is huge and will only grow.

3. Stablecoins

There are 3 types of stablecoins:

a) USD-backed: backed by a real-USD and as such the most safe and secure stablecoin.

b) Crypto-collateralized: by locking up one’s crypto, similarly to how I described earlier, one can take out decentralized stablecoins as a loan. The most common is DAI which is issued by MakerDAO.

c) Algorithmic: these attempt to maintain their pegs through various market incentives. While being capital efficient, they are relatively new and several have failed, most famously Terra Luna’s UST.

USD-backed stablecoins have the most immediate use cases such as enabling the instantaneous transfer of funds globally. This has massive implications on for remittances, payments, payroll, etc. Additionally, they provide a means for users to hedge against inflation. For example, Argentinians purchase USD stablecoins to hedge against inflation in a permissionless manner, considering restrictions imposed by their governments.

In the future, I expect that brands such as Amazon will prefer to be paid in “Amazon Dollars” for example in order to avoid payment processing fees, and to provide creative marketing incentives towards token holders. It’s expected that upcoming U.S. legislation on stablecoins will prohibit them from launching their own stablecoins, so they’ll likely have to rely on stablecoin infrastructure companies.

Conclusion

Decentralized Finance is a rapidly growing industry with constant innovation. There have been many failures in the past that have hurt users, such as the fall of Terra Luna.

At the same time, many tangible benefits are already realizable through the use of blockchain technology, already unlocking real benefits for global users. Above I described three such examples, but there are many more that I highly encourage readers to explore.

As the reader, what do you think is most impactful? Is there anything you think should have been covered? Please let me know in the comments 🙂